The Iran Tax Administration issued Circular 200/90783 (dated 1404/11/18, 2026-02-07) on the waiver of waivable tax penalties. Later, Circular 200/93750 (dated 1404/11/28, 2026-02-17) extended the payment deadline required to benefit from the waiver. The extended deadline is 1404/12/14 (2026-03-05). A clarification letter (200/91050, dated 1404/11/19, 2026-02-08) confirms that waiver requests are submitted via my.tax.gov.ir.

1) Main circular: 200/90783 1404/11/18 | 2026-02-07

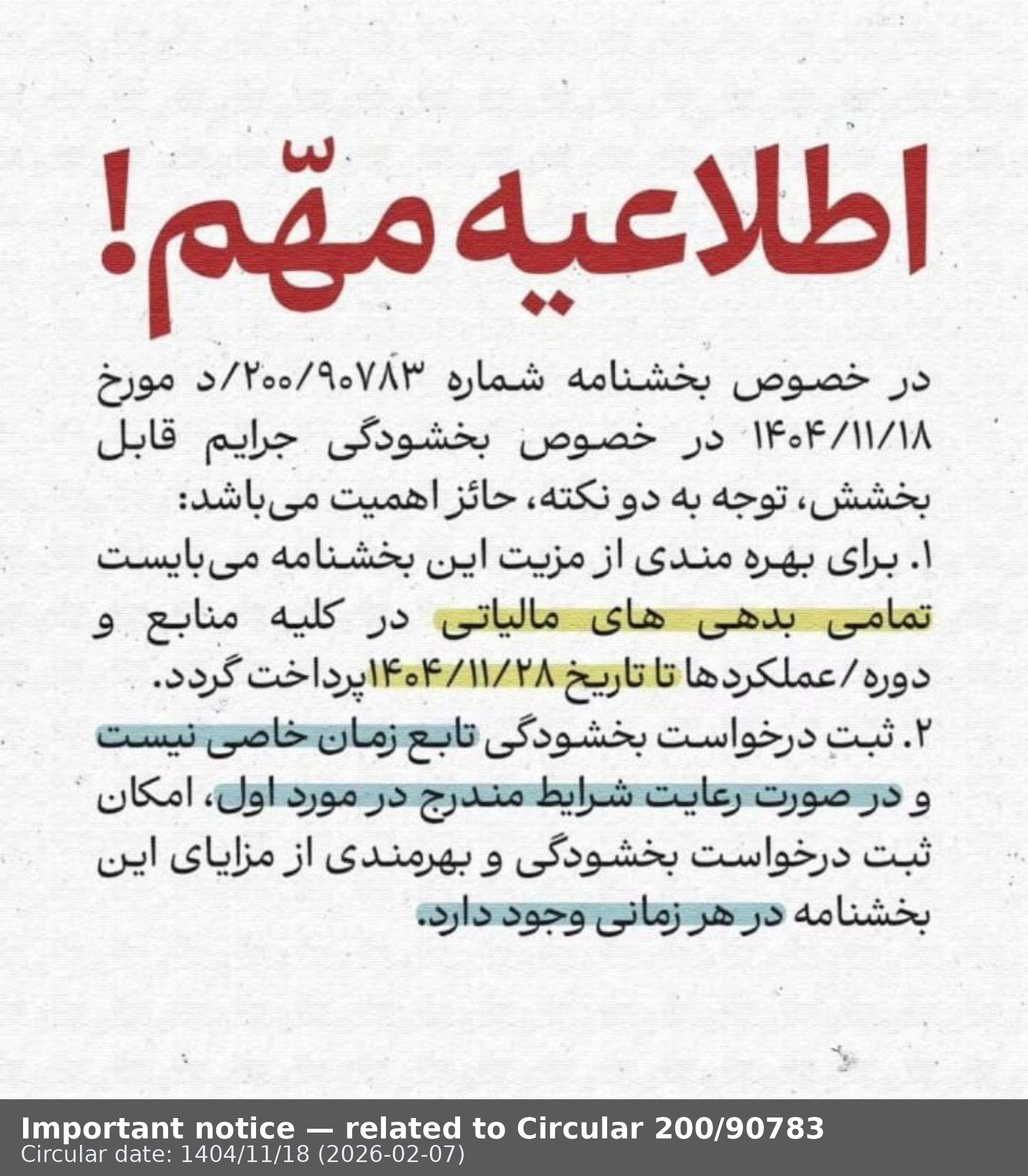

- Topic: waiver of waivable tax penalties under the applicable rules.

- To benefit, taxpayers must meet the settlement/payment condition for their tax liabilities (see the attached notice).

- After meeting the conditions, the waiver request can be registered in the system.

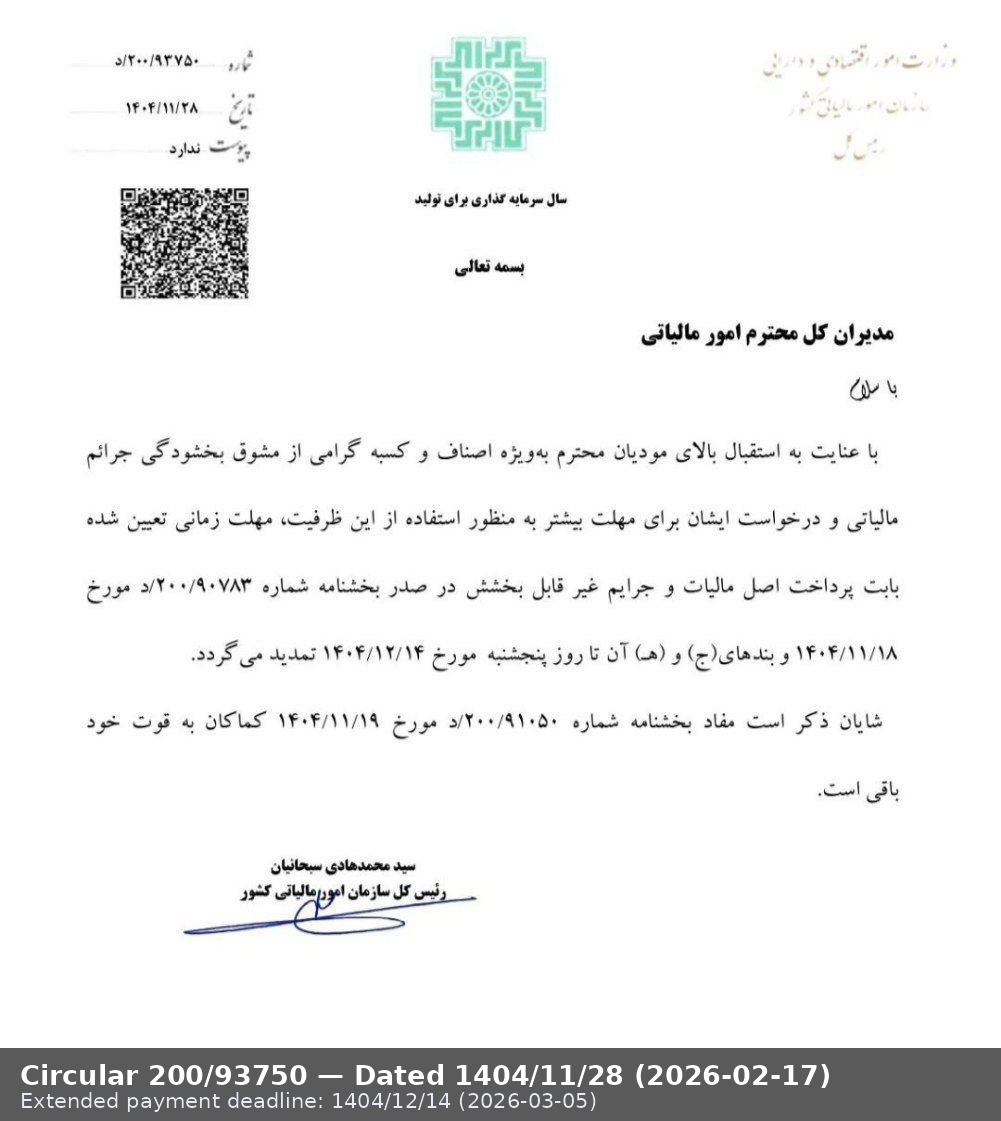

2) Deadline extension: 200/93750 1404/11/28 | 2026-02-17

- The payment deadline for principal tax and non-waivable penalties was extended.

- Deadline: 1404/12/14 (2026-03-05).

- The letter states that the clarification letter 200/91050 remains in effect.

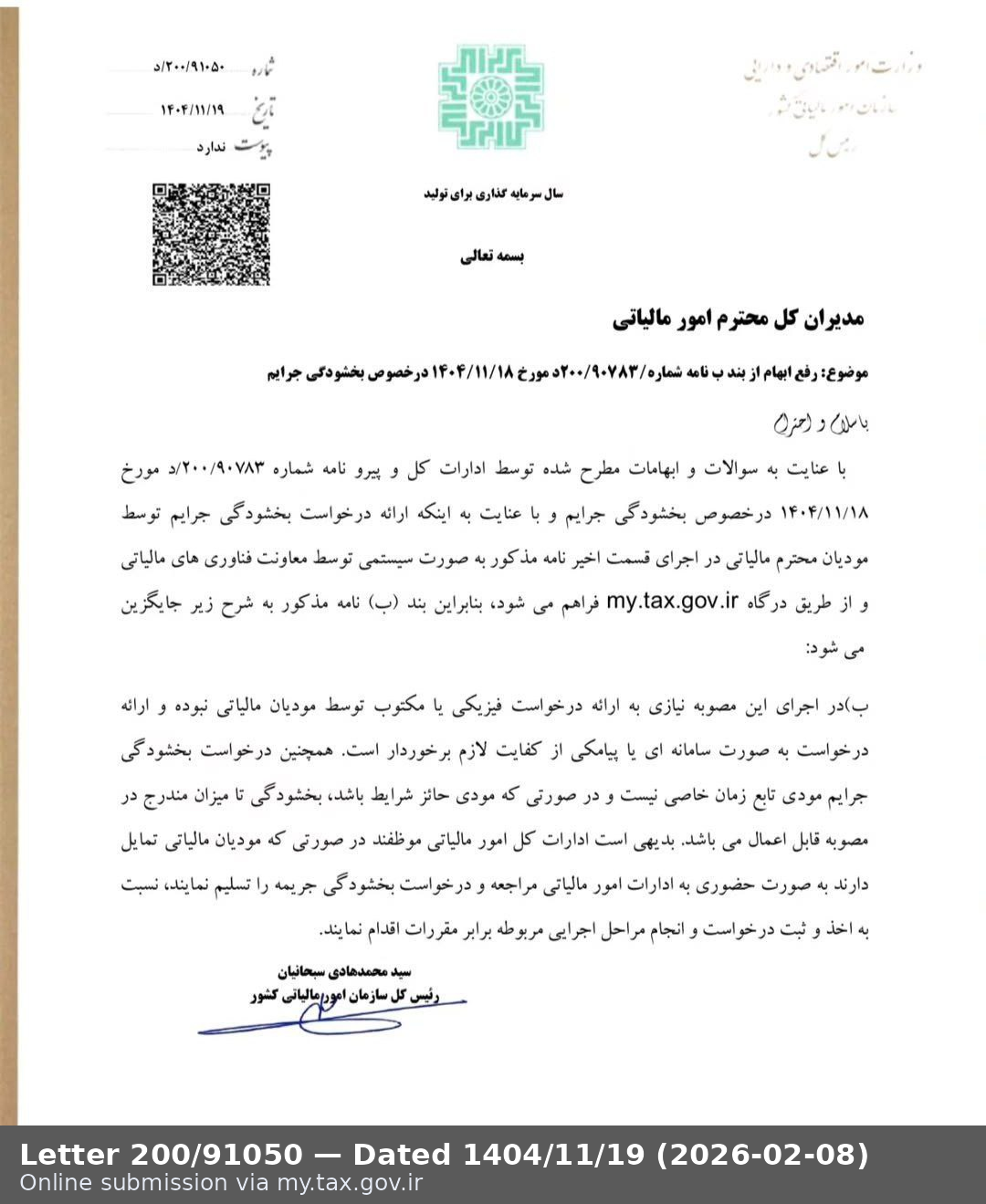

3) Online submission my.tax.gov.ir

- Based on letter 200/91050 (1404/11/19 | 2026-02-08), the waiver workflow is available digitally.

- In many cases, a digital submission is sufficient unless follow-up is requested.

4) Key prerequisite

- The decisive factor is meeting the payment/settlement condition by 1404/12/14 (2026-03-05).

- The attached notice explains this operational point in detail.

Key dates at a glance

- Circular 200/90783: 1404/11/18 (2026-02-07)

- Letter 200/91050: 1404/11/19 (2026-02-08)

- Circular 200/93750: 1404/11/28 (2026-02-17)

- Payment deadline: 1404/12/14 (2026-03-05)

The official attachments are scans of the original documents.

How to register the waiver request (high level)

- Ensure the required liabilities are settled/paid by 1404/12/14 (2026-03-05).

- Log in to my.tax.gov.ir and register the waiver request using the available workflow.

- Monitor the status in the portal and follow up with the tax office if the system requests additional action.

Official attachments